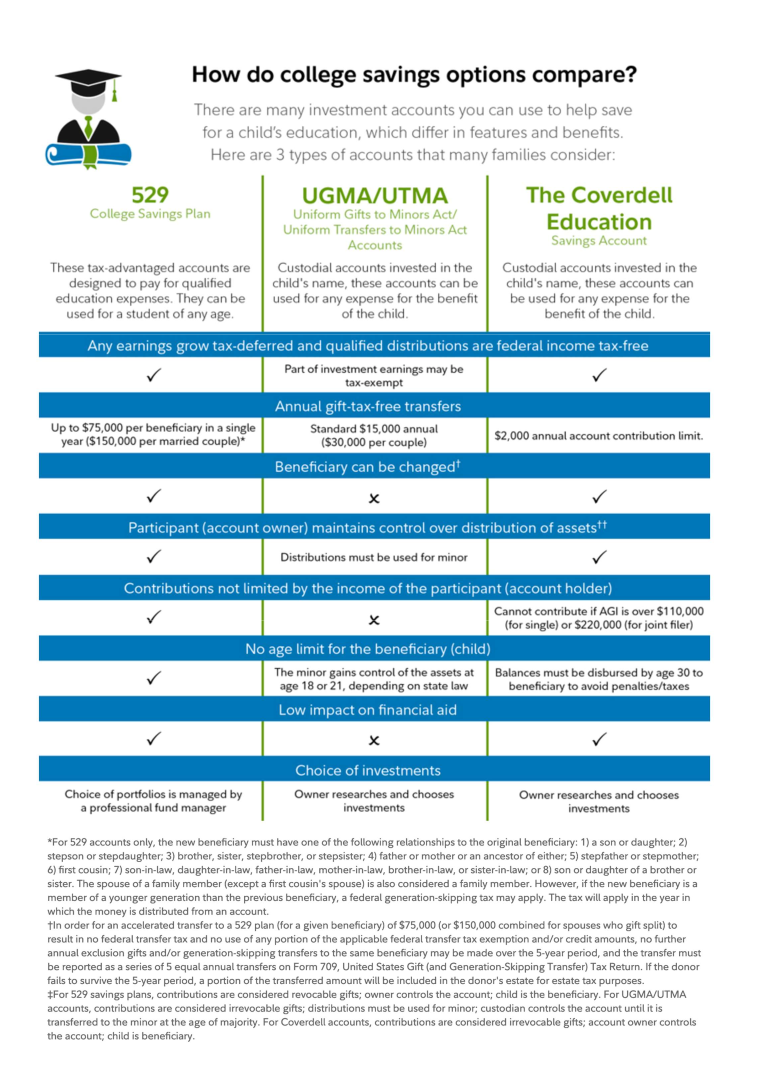

529 College Savings Withdrawals

Did you know that 529 Plan Savings can now be used for much more than college? You can benefit from tax-free investment growth in a 529 plan for K-12 tuition, apprenticeships, student loan repayments, and (as of January 1, 2024) you can also use the funds for Roth IRA rollovers to fund tax-free retirement savings.

The following qualified withdrawals can be taken from 529 savings with no tax or penalties:

K-12 Tuition Expenses – $10,000 annual limit per beneficiary.

College expenses for tuition and fees, books and materials, room and board (if enrolled at least half-time), computers and related equipment, internet access, and other expenses deemed “required for enrollment” by the college.

- The college must be recognized as an “eligible” institution. You can look up your school here: Saving for College: Is you institution 529 eligible?

Cost of qualified apprenticeship program expenses (fees, supplies, equipment).

- The apprenticeship program must be registered with the US DOL’s National Apprenticeship Act to qualify.

- Apprenticeship USA Job Finder

Student Loan Repayments – $10,000 lifetime limit for each beneficiary and the beneficiary’s siblings. (Qualified education loans include all federal student loans and many private student loans.

- Account owners may also change the beneficiary to themselves if they want to repay their own student loan).

529-to-Roth rollovers up to $35,000 lifetime per beneficiary, subject to annual Roth contribution limits. (State income tax might apply for some states/plans)

Helpful Tips:

If you have more than one 529 plan, take qualified distributions from the account with the highest growth rate first.

Whenever possible, try to pay all qualified expenses directly from the plan. (i.e. have the plan send tuition and room and board payments directly to the school.)

Qualified withdrawals – If you pay for expenses out of pocket for reimbursement, you must take care to take the 529 withdrawal in the same calendar year that the expense is incurred. Best practice – to avoid any issues matching the withdrawal timing with the expense, try to pay qualified expenses directly from the 529 account. Instruct the 529 plan to send payments for tuition, fees, room and board directly to the school, for example.

Non-Qualified Expenses – you cannot use the 529 funds for extracurricular activities, such as club sports and fraternity or sorority activities, college application and testing fees, transportation and travel costs (unless deemed required for attendance by the college).

Taxes and Penalties for Non-Qualifed Withdrawals – If you take withdrawals for non-qualified expenses, or if your withdrawal for an otherwise qualified expense is taken in the wrong calendar year, the earnings/growth portion of the withdrawal is included in your taxable income and taxed at your marginal tax rate plus a 10% penalty. State taxes and penalities may also apply based on the filing state for the taxpayer (can be reported by either the account holder or the beneficiary).

Click here to download the doc to learn more…

Sources:

Saving for College: What is a 529 Plan?

As of 8/21/2024